Is there a catch-up contribution limit for IRAs in 2024? Absolutely! If you’re 50 or older, you can contribute an extra amount to your IRA to help boost your retirement savings. This guide will break down everything you need to know about catch-up contributions, from eligibility requirements to the potential tax benefits.

The catch-up contribution limit allows individuals aged 50 and over to contribute an additional amount to their traditional or Roth IRAs, on top of the regular contribution limit. This extra contribution can significantly accelerate your retirement savings, potentially putting you in a better financial position later in life.

Contents List

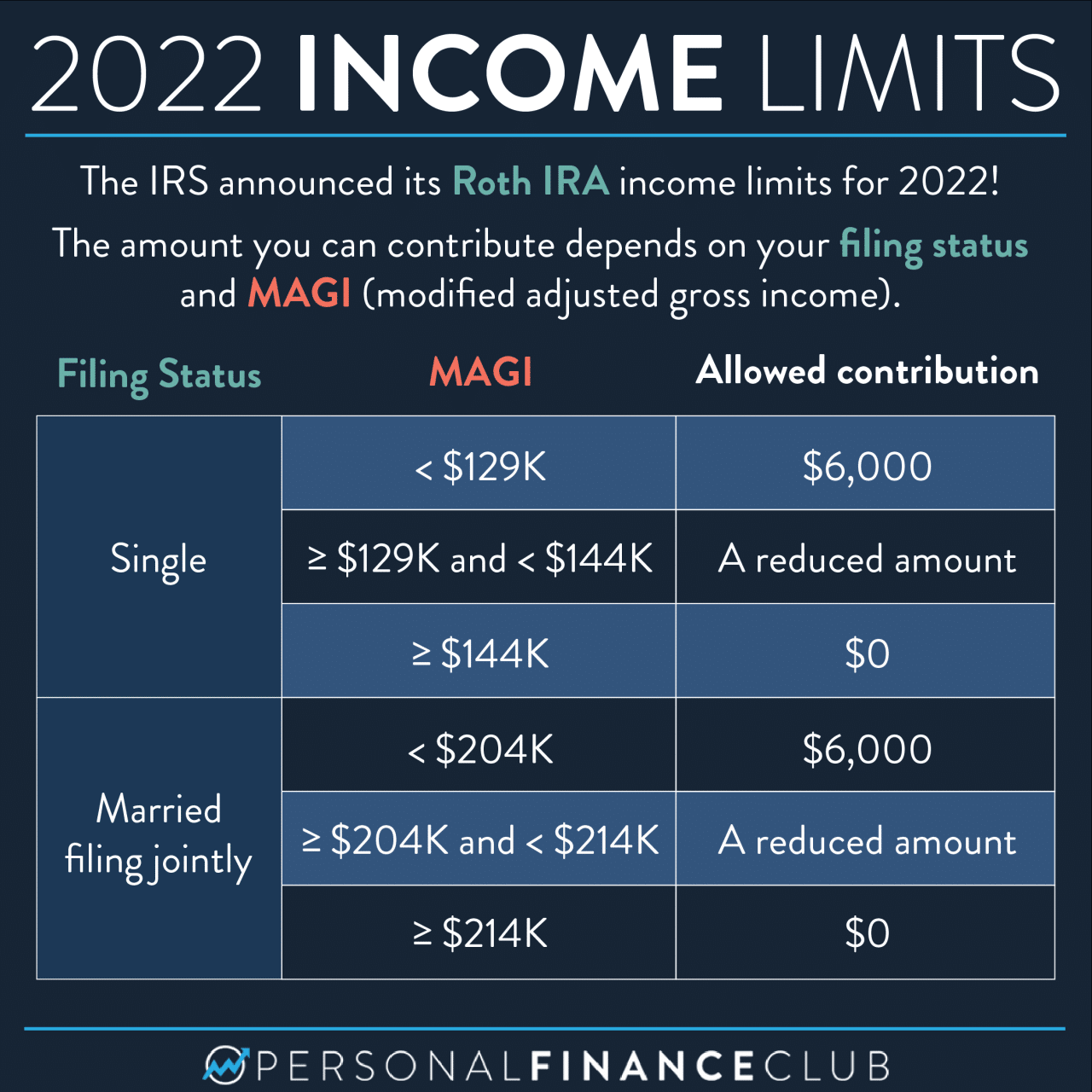

IRA Contribution Limits in 2024

The amount you can contribute to an IRA each year is limited. These limits are set by the IRS and are adjusted annually to reflect inflation. The 2024 IRA contribution limits are designed to help individuals save for retirement.

If you’re planning on driving for business purposes in October 2024, you might be wondering when the mileage rate will be updated. This rate, set by the IRS, is used to calculate deductible expenses for business travel.

Contribution Limits for 2024

The maximum amount you can contribute to a traditional or Roth IRA in 2024 is $7,000. This limit applies to both traditional and Roth IRAs.

Catch-up Contributions for Those Aged 50 and Over in 2024

If you are 50 years old or older in 2024, you can make an additional catch-up contribution to your IRA. The catch-up contribution limit for 2024 is $1,500. This means that you can contribute up to $8,500 to your IRA in 2024 if you are 50 or older.

Saving for retirement is important, and knowing your contribution limits is crucial. The IRA contribution limits for 2024 and 2025 are subject to change, so it’s best to stay informed.

Traditional and Roth IRA Contribution Limits in 2024

Here is a table that summarizes the contribution limits for traditional and Roth IRAs in 2024:

| IRA Type | Contribution Limit | Catch-up Contribution Limit (Age 50+) |

|---|---|---|

| Traditional IRA | $7,000 | $1,500 |

| Roth IRA | $7,000 | $1,500 |

It is important to note that these contribution limits are subject to change. It is always best to consult with a qualified financial advisor to determine the best course of action for your individual circumstances.

Maximizing your retirement contributions is important. Learn about the maximum 401k contribution for 2024 to ensure you’re taking advantage of all available savings options.

Eligibility for Catch-Up Contributions

Catch-up contributions are a great way for those over 50 to boost their retirement savings. They allow you to contribute an extra amount to your IRA each year, on top of the regular contribution limit. However, there are some eligibility requirements you need to meet to take advantage of this benefit.

The IRS mileage rate is an important factor for business travel expenses. Learn about the IRS mileage rate for October 2024 to ensure accurate deductions.

Age Requirement, Is there a catch-up contribution limit for IRAs in 2024

To be eligible for catch-up contributions, you must be at least 50 years old by the end of the tax year. This means you can start making catch-up contributions in the year you turn 50, even if you haven’t reached your 50th birthday yet.

Tax brackets and thresholds can change annually. Make sure you’re aware of the tax bracket thresholds for 2024 to understand your tax liability.

Income Limitations

There are no income limitations for catch-up contributions to traditional or Roth IRAs. This means that regardless of your income, you can contribute the full catch-up amount if you meet the age requirement.

Catch-Up Contributions for Traditional and Roth IRAs

If you contribute to both a traditional IRA and a Roth IRA, the catch-up contribution limit applies to the total amount you contribute to both accounts. For example, if you are 50 years old and the catch-up contribution limit is $1,000, you can contribute up to $7,500 to a traditional IRA and $1,000 to a Roth IRA, for a total of $8,500.

Benefits of Catch-Up Contributions

Catch-up contributions offer a valuable opportunity for individuals approaching retirement to significantly boost their savings. These contributions provide tax advantages and allow individuals to accelerate their retirement savings, ultimately increasing their financial security during their golden years.

If you’re self-employed, you may have a SEP IRA. Check out the IRA contribution limits for SEP IRA in 2024 to understand your retirement savings options.

Tax Benefits of Catch-Up Contributions

Catch-up contributions to IRAs offer valuable tax benefits, potentially leading to significant savings on your tax bill. These benefits stem from the tax-deferred nature of traditional IRAs and the tax-free growth of Roth IRAs.

If you’re a freelancer or contractor, you’ll likely need to fill out a W9 form. Learn how to fill out a W9 form for October 2024 to ensure you’re providing the correct information to your clients.

- Traditional IRAs:Contributions to traditional IRAs are tax-deductible, meaning you can deduct the amount of your contributions from your taxable income, reducing your tax liability for the current year. The taxes on your earnings and withdrawals are deferred until retirement, potentially reducing your tax burden in your later years.

Self-employment comes with unique retirement savings options. Check out the IRA contribution limits for self-employed in 2024 to maximize your retirement savings.

- Roth IRAs:While Roth IRA contributions are not tax-deductible, the earnings and withdrawals during retirement are tax-free. This can be advantageous if you anticipate being in a higher tax bracket during retirement than you are now. By making Roth IRA contributions, you can avoid paying taxes on your retirement income.

Retirement planning is essential, and knowing how much you can contribute to your IRA is a key factor. Find out how much you can contribute to your IRA in 2024 to make the most of your retirement savings.

Accelerating Retirement Savings with Catch-Up Contributions

Catch-up contributions are designed to help individuals nearing retirement age accelerate their savings. By making additional contributions beyond the regular contribution limits, you can significantly boost your retirement nest egg.

If you’re looking to contribute to your IRA, you might wonder what the maximum IRA contribution for 2024 is. Knowing this limit can help you plan your retirement savings.

“The catch-up contribution provision in IRAs allows individuals to contribute an additional amount to their retirement savings, helping them make up for lost time and potentially reach their retirement goals faster.”

Retirement planning is an important part of financial planning. Knowing how much you can contribute to your 401k in 2024 can help you set realistic savings goals.

Strategies for Maximizing Catch-Up Contribution Benefits

Maximizing the benefits of catch-up contributions requires a strategic approach.

Self-employed individuals have unique retirement savings options. Find out about the 401k contribution limits for 2024 for self-employed to make informed decisions about your retirement savings.

- Contribute the maximum amount:If you are eligible, contribute the maximum catch-up contribution amount allowed each year. This will significantly boost your retirement savings.

- Start early:While catch-up contributions are designed for those nearing retirement, starting earlier can still be beneficial. The earlier you start, the more time your investments have to grow, leading to a larger nest egg.

- Consider a Roth IRA:If you anticipate being in a higher tax bracket during retirement, consider contributing to a Roth IRA. This can help you avoid paying taxes on your retirement income.

- Diversify your investments:Diversify your investments within your IRA to manage risk and potentially maximize returns. This can help you achieve your retirement goals even during market fluctuations.

Example Scenarios

Let’s illustrate how catch-up contributions work with some practical examples.

Total Contribution Limits for Different Ages

The following table shows the total contribution limit for individuals aged 49 and 52 in 2024:

| Age | Traditional IRA Contribution Limit | Roth IRA Contribution Limit |

|---|---|---|

| 49 | $7,500 | $7,500 |

| 52 | $8,500 | $8,500 |

Potential Tax Savings with Catch-Up Contributions

Imagine a 52-year-old individual earning $100,000 annually and contributing the maximum amount to their traditional IRA in 2024. Assuming a tax bracket of 24%, their contribution of $8,500 would reduce their taxable income by $8,500, leading to a tax savings of $2,040 ($8,500 x 0.24).

If you’re a high earner, you might be wondering about the 401k contribution limits for 2024 for high earners. These limits can affect how much you can contribute to your retirement savings plan.

Catch-Up Contributions vs. Other Retirement Savings Strategies

A 50-year-old individual with a 401(k) plan and a traditional IRA can choose between making catch-up contributions to their 401(k) or their traditional IRA. Here’s a comparison:* 401(k) Catch-Up Contributions:The individual can contribute an additional $8,500 to their 401(k) in 2024. This could offer a higher potential return due to the potential for employer matching and lower fees.

However, contributions are taxed when withdrawn in retirement.

Moving can be a big expense, and the IRS allows you to deduct certain moving costs. Knowing the October 2024 mileage rate for moving expenses can help you calculate your deductions accurately.

Traditional IRA Catch-Up Contributions

Depending on your age, the amount you can contribute to your IRA may vary. Check out the IRA contribution limits for 2024 by age to ensure you’re maximizing your retirement savings.

The individual can contribute an additional $1,000 to their traditional IRA in 2024. This may provide more flexibility for retirement planning, as traditional IRA withdrawals are generally tax-deductible.The best strategy depends on individual circumstances, such as income level, employer matching, and investment goals.

Consulting with a financial advisor can help determine the most beneficial approach.

Summary

Catch-up contributions can be a powerful tool for those looking to maximize their retirement savings. By understanding the rules and benefits, you can make informed decisions about your retirement planning and potentially enjoy a more comfortable retirement. However, it’s important to consider the tax implications of both contributions and withdrawals, and to consult with a financial advisor to determine the best strategy for your individual circumstances.

Frequently Asked Questions: Is There A Catch-up Contribution Limit For IRAs In 2024

What is the catch-up contribution limit for 2024?

For 2024, the catch-up contribution limit for individuals aged 50 and over is $1,000. This means that in addition to the regular contribution limit of $6,500, you can contribute an extra $1,000 to your IRA.

Can I contribute to both a traditional and Roth IRA with catch-up contributions?

Yes, you can contribute to both a traditional and Roth IRA with catch-up contributions. However, the total amount you contribute to both types of IRAs combined cannot exceed the total contribution limit for the year.

How do catch-up contributions affect my taxes?

Catch-up contributions to a traditional IRA are tax-deductible, meaning they can reduce your taxable income in the current year. Catch-up contributions to a Roth IRA are not tax-deductible, but your withdrawals in retirement will be tax-free.

What are the potential drawbacks of catch-up contributions?

While catch-up contributions can be beneficial, there are some potential drawbacks. For example, if you withdraw funds from your IRA before age 59 1/2, you may be subject to a 10% early withdrawal penalty, in addition to regular taxes.