Annuity Options 2024 offer a compelling path to secure retirement income, but navigating the complexities of this market requires careful consideration. With interest rates fluctuating and new products emerging, understanding your options is paramount. This guide explores the diverse landscape of annuities, outlining the benefits, drawbacks, and factors to consider when making informed decisions.

From fixed annuities to variable and indexed options, the world of annuities offers a range of choices to suit different risk profiles and financial goals. We delve into the latest trends, popular products, and tax implications to empower you with the knowledge needed to make the best choice for your unique circumstances.

Contents List

Introduction to Annuities

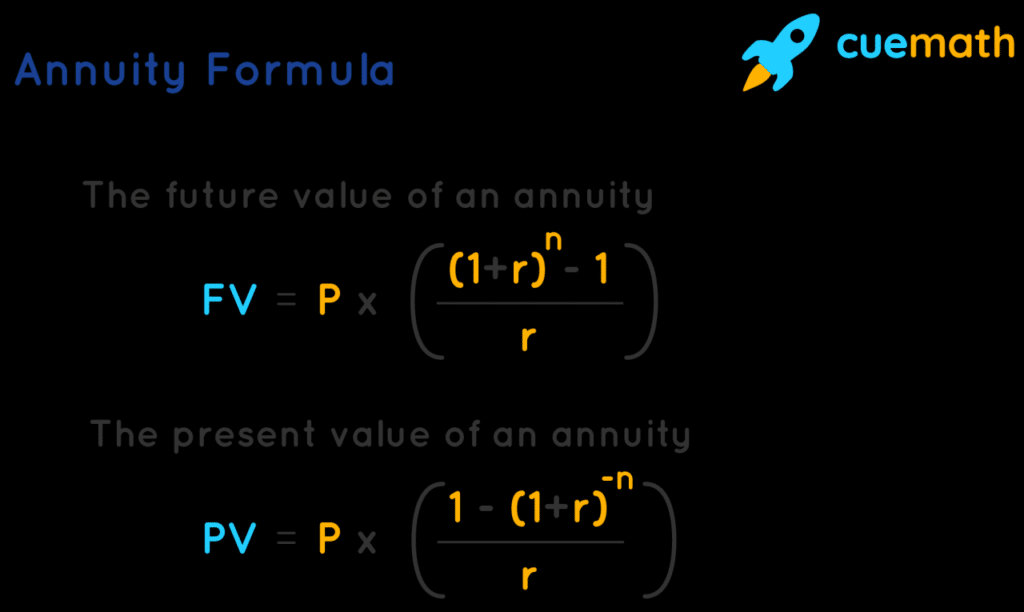

Annuities are financial products designed to provide a stream of regular payments over a specified period, typically during retirement. They are often used as a part of retirement planning to ensure a steady income stream during the golden years. Annuities can be purchased from insurance companies, and they work by pooling funds from multiple individuals and investing them in various assets.

The investment returns, along with the principal, are then used to generate the annuity payments.

Types of Annuities

Annuities come in different forms, each with its own characteristics and suitability for different financial goals and risk tolerances.

- Fixed Annuities: These offer guaranteed interest rates and fixed payments for a specific period. They provide predictable income, but the returns may not keep pace with inflation.

- Variable Annuities: These link payments to the performance of underlying investments, such as mutual funds. They offer the potential for higher returns but also carry investment risk.

- Indexed Annuities: These offer a return linked to the performance of a specific index, such as the S&P 500. They provide potential growth while limiting downside risk.

Benefits of Annuities

Annuities can offer several benefits, including:

- Guaranteed Income Stream: Annuities provide a steady stream of income, which can be crucial for retirees.

- Protection Against Outliving Savings: Annuities can help ensure that your savings last throughout your retirement.

- Tax Advantages: Some annuities offer tax-deferred growth, meaning that taxes are not paid until withdrawals are made.

- Death Benefit: Some annuities offer a death benefit, which can provide a lump sum payment to beneficiaries upon the annuitant’s death.

Drawbacks of Annuities

While annuities offer several benefits, they also have some drawbacks, including:

- Limited Liquidity: Accessing your funds before the annuity’s start date can be restricted, and early withdrawals may incur penalties.

- Fees and Charges: Annuities often involve fees and charges, which can impact returns.

- Potential for Loss of Principal: Variable and indexed annuities carry investment risk, and there is a potential for losing principal.

Annuity Options in 2024

The annuity market is constantly evolving, with new products and features emerging regularly. In 2024, several factors are shaping the annuity landscape, including interest rate fluctuations, market volatility, and evolving consumer preferences.

Latest Trends and Developments

The annuity market is witnessing several trends in 2024, driven by evolving investor needs and market conditions.

- Increased Demand for Guaranteed Income: As individuals seek financial security in retirement, demand for guaranteed income products, such as fixed annuities, is on the rise.

- Focus on Longevity Risk: With people living longer, there is an increasing focus on longevity risk, and annuities can provide protection against outliving savings.

- Innovation in Product Design: Annuity providers are introducing innovative products, such as hybrid annuities, which combine features of fixed and variable annuities.

Current Interest Rate Environment

Interest rates play a crucial role in annuity returns. In 2024, the Federal Reserve has been raising interest rates to combat inflation. This rising interest rate environment can impact annuities in several ways:

- Higher Guaranteed Rates: Fixed annuities typically offer higher guaranteed rates in a rising interest rate environment.

- Increased Competition: The rising interest rate environment can lead to increased competition among annuity providers, potentially resulting in more favorable rates for consumers.

- Impact on Variable Annuities: Rising interest rates can affect the performance of underlying investments in variable annuities.

New Annuity Products and Features

Annuity providers are constantly introducing new products and features to meet evolving consumer needs. Some notable examples in 2024 include:

- Enhanced Death Benefit Options: Some annuities offer more flexible death benefit options, allowing beneficiaries to choose how they receive the death benefit.

- Income Riders: These riders can provide additional income streams during retirement, such as guaranteed lifetime income.

- Annuities with Living Benefits: These annuities offer benefits during the annuitant’s lifetime, such as protection against market downturns or guaranteed minimum income.

Factors to Consider When Choosing an Annuity

Choosing the right annuity requires careful consideration of various factors to ensure it aligns with your financial goals and risk tolerance. Several key factors to consider include:

Age and Risk Tolerance

Your age and risk tolerance are crucial factors in annuity selection. Younger individuals with a longer time horizon may be more comfortable with variable annuities, while older individuals may prefer the stability of fixed annuities.

Financial Goals

Your financial goals will determine the type of annuity that best suits your needs. If you seek guaranteed income, a fixed annuity might be suitable. If you want potential for growth, a variable annuity might be more appropriate.

Tax Implications

Tax implications are a critical factor in annuity selection. Some annuities offer tax-deferred growth, while others do not. Understanding the tax treatment of annuity income and withdrawals is essential.

Other Considerations

Other factors to consider include:

- Fees and Charges: Compare fees and charges across different annuity products.

- Minimum Investment Requirements: Some annuities have minimum investment requirements.

- Withdrawal Options: Understand the withdrawal options and any penalties associated with early withdrawals.

- Death Benefit: Consider the death benefit options and how they align with your estate planning goals.

Consulting with a Financial Advisor

It is highly recommended to consult with a qualified financial advisor before purchasing an annuity. A financial advisor can help you assess your financial situation, understand your goals, and choose the annuity that best suits your needs.

Popular Annuity Products in 2024

The annuity market offers a wide range of products, each with its own features, benefits, and risks. Here are some popular annuity products available in 2024:

Fixed Annuities

Fixed annuities provide guaranteed interest rates and fixed payments for a specific period. They offer predictable income and are suitable for individuals seeking stability and guaranteed returns.

Variable Annuities

Variable annuities link payments to the performance of underlying investments, such as mutual funds. They offer the potential for higher returns but also carry investment risk. Variable annuities are suitable for individuals with a higher risk tolerance and a longer time horizon.

Indexed Annuities

Indexed annuities offer a return linked to the performance of a specific index, such as the S&P 500. They provide potential growth while limiting downside risk. Indexed annuities are suitable for individuals seeking growth potential with some downside protection.

Hybrid Annuities

Hybrid annuities combine features of fixed and variable annuities. They offer a balance between guaranteed income and growth potential. Hybrid annuities are suitable for individuals seeking a combination of stability and potential for growth.

Annuity Products Comparison, Annuity Options 2024

| Product Name | Type | Features | Minimum Investment | Potential Returns |

|---|---|---|---|---|

| Fixed Annuity | Fixed | Guaranteed interest rates, fixed payments | $5,000

|

Lower but guaranteed returns |

| Variable Annuity | Variable | Investment options, potential for growth | $10,000

|

Higher potential returns but with investment risk |

| Indexed Annuity | Indexed | Linked to market index, potential for growth with downside protection | $5,000

|

Moderate potential returns with limited downside risk |

| Hybrid Annuity | Hybrid | Combines features of fixed and variable annuities | $10,000

|

Balanced approach with both guaranteed income and growth potential |

Tax Implications of Annuities

Understanding the tax implications of annuities is crucial for making informed financial decisions. The tax treatment of annuity income and withdrawals can vary depending on the type of annuity and the specific terms of the contract.

Tax Treatment of Annuity Income

Annuity income is typically taxed as ordinary income. This means that the payments you receive from an annuity will be subject to federal and state income tax rates. The amount of income that is taxed depends on the type of annuity and the specific terms of the contract.

Tax Advantages of Annuities

Annuities can offer some tax advantages, such as:

- Tax-Deferred Growth: Some annuities allow for tax-deferred growth, meaning that taxes are not paid until withdrawals are made.

- Tax-Free Death Benefit: Some annuities offer a tax-free death benefit to beneficiaries.

Tax Disadvantages of Annuities

Annuities can also have some tax disadvantages, such as:

- Taxable Withdrawals: Withdrawals from annuities are typically taxable as ordinary income.

- Early Withdrawal Penalties: Early withdrawals from annuities may be subject to penalties.

Tax Implications and Annuity Choices

The tax implications of annuities can significantly impact your overall financial planning. Consulting with a tax advisor or financial professional can help you understand the tax treatment of specific annuity products and how they might affect your tax liability.

Risks and Considerations

Annuities, while offering potential benefits, also carry inherent risks. Understanding these risks and carefully considering the terms of the annuity contract is crucial before making a decision.

Potential Risks Associated with Annuities

The potential risks associated with annuities include:

- Loss of Principal: Variable and indexed annuities carry investment risk, and there is a potential for losing principal.

- Limited Liquidity: Accessing your funds before the annuity’s start date can be restricted, and early withdrawals may incur penalties.

- Fees and Charges: Annuities often involve fees and charges, which can impact returns.

- Inflation Risk: Fixed annuities may not keep pace with inflation, eroding the purchasing power of your payments.

- Company Risk: The financial stability of the insurance company issuing the annuity is a risk factor.

Importance of Understanding Contract Terms

It is essential to carefully read and understand the terms and conditions of the annuity contract before purchasing an annuity. The contract will Artikel the specific features, benefits, risks, and limitations of the product. It is advisable to seek professional advice to ensure you fully understand the contract and its implications.

Mitigating Potential Risks

While some risks are inherent to annuities, you can take steps to mitigate potential risks, such as:

- Diversify Your Investments: If you choose a variable annuity, diversify your investments across different asset classes to reduce risk.

- Choose a Reputable Insurance Company: Select an insurance company with a strong financial track record.

- Consult with a Financial Advisor: A financial advisor can help you understand the risks and choose an annuity that aligns with your financial goals and risk tolerance.

Annuity Alternatives: Annuity Options 2024

While annuities can be a valuable tool for retirement planning, they are not the only option. Several alternative investment options may be suitable for retirement savings.

Alternative Investment Options

Some alternative investment options for retirement planning include:

- Individual Retirement Accounts (IRAs): IRAs offer tax advantages for retirement savings, with both traditional and Roth IRA options available.

- 401(k) Plans: Employer-sponsored retirement plans offer tax-advantaged savings opportunities.

- Mutual Funds: Mutual funds provide diversification and professional management, allowing investors to access a variety of asset classes.

- Exchange-Traded Funds (ETFs): ETFs are similar to mutual funds but are traded on stock exchanges, offering greater flexibility and lower fees.

- Real Estate: Real estate investments can offer potential for appreciation and rental income.

Comparison of Annuities and Alternatives

Annuities and alternative investment options have their own advantages and disadvantages. When choosing between these options, consider factors such as:

- Risk Tolerance: Annuities offer different levels of risk, while alternative options vary in their risk profiles.

- Tax Implications: Annuities and alternative investments have different tax implications, which can impact your overall financial planning.

- Liquidity: Some annuities have limited liquidity, while other investment options offer greater flexibility.

- Fees and Charges: Compare fees and charges across different investment options.

Wrap-Up

As you embark on your retirement planning journey, remember that annuities can be a valuable tool, but they are not a one-size-fits-all solution. Carefully evaluate your individual needs, risk tolerance, and financial goals before making any decisions. Consult with a qualified financial advisor to personalize your strategy and ensure you’re on the right path toward a secure and comfortable retirement.

Questions Often Asked

What is the minimum investment required for an annuity?

Minimum investment requirements vary depending on the specific annuity product and the issuing insurance company. It’s best to check with the provider directly for their specific requirements.

Can I withdraw money from an annuity before retirement?

Some annuities allow for partial withdrawals, but there may be penalties or restrictions depending on the type of annuity and the terms of the contract. It’s crucial to review the contract details before making any withdrawals.

Are annuities guaranteed?

The guarantee associated with an annuity depends on the type of annuity. Fixed annuities typically offer guaranteed interest rates and principal protection, while variable annuities carry investment risk. It’s essential to understand the specific guarantees associated with each annuity product.