Is Annuity Bond 2024 the right investment for you? This comprehensive guide delves into the world of annuity bonds, exploring their intricacies, benefits, risks, and current market trends. We’ll unpack the different types of annuity bonds available, analyze investment strategies, and examine the regulatory landscape surrounding these financial instruments.

Annuity bonds offer a unique approach to investment, combining the security of bonds with the potential for growth. They can be a valuable addition to a diversified portfolio, providing income and potential capital appreciation. However, understanding the risks and complexities of annuity bonds is crucial before making any investment decisions.

Contents List

Annuity Bonds: An Overview

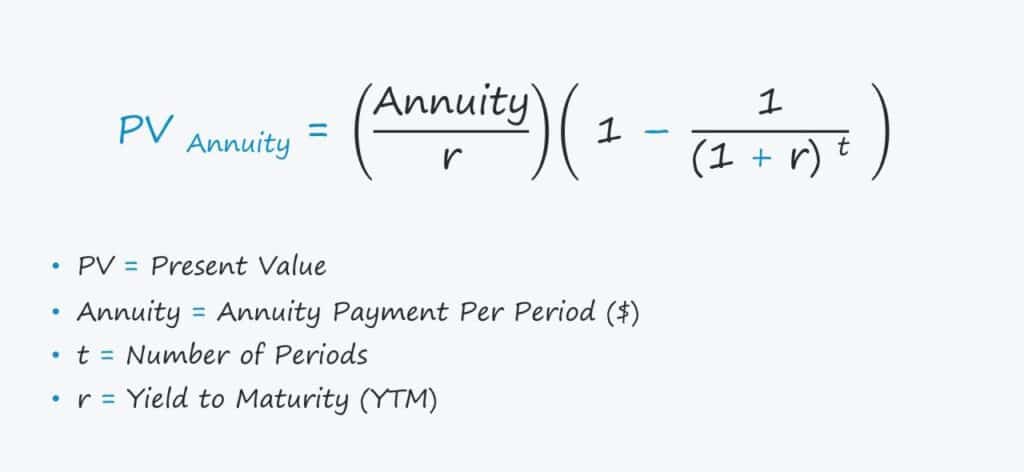

Annuity bonds are a type of investment that offers a guaranteed stream of income for a specific period of time. They are often considered a safe and reliable way to generate regular income, especially for retirees or those seeking to supplement their retirement income.

Keeping your Android device secure is essential, and regular security updates are crucial. You can find information about the latest Android WebView 202 security updates online. For those interested in becoming a delivery driver, the Glovo app delivery driver earnings and tips article provides insights.

What are Annuity Bonds?

Annuity bonds are financial instruments that provide a guaranteed stream of payments, typically in the form of fixed monthly or annual installments, for a specified period. These bonds are issued by insurance companies and are backed by their financial strength and assets.

The payments are generally made for the life of the bondholder or for a predetermined term.

Key Features of Annuity Bonds

Annuity bonds possess distinct characteristics that set them apart from other investments:

- Guaranteed Income:Annuity bonds offer a fixed and predictable income stream, providing financial security and stability.

- Principal Protection:In most cases, the principal invested in an annuity bond is protected from market fluctuations and losses.

- Tax Advantages:Depending on the type of annuity bond, certain tax benefits may be available, such as tax-deferred growth or tax-free income.

- Flexibility:Some annuity bonds offer options for customization, such as the payment frequency or the length of the payout period.

Definition of Annuity Bonds

An annuity bond is a type of investment that provides a guaranteed stream of income payments for a specific period, typically in exchange for a lump-sum payment or a series of payments. These bonds are issued by insurance companies and are backed by their financial strength and assets, offering a secure and predictable source of income for investors.

The latest Snapdragon chipsets are set to power laptops, with the Snapdragon 2024 for laptops promising impressive performance and efficiency. You can find out more about its release date and pricing here.

Types of Annuity Bonds

Annuity bonds come in various forms, each with its own set of features, benefits, and risks. Understanding the different types available is crucial for selecting the most suitable option for your investment goals.

Classifying Annuity Bonds

Annuity bonds can be categorized based on several factors, including the payment structure, the investment period, and the level of risk involved. Here are some common types of annuity bonds:

| Type | Features | Benefits | Risks |

|---|---|---|---|

| Fixed Annuity | Guaranteed fixed interest rate, predictable payments | Stable income, principal protection | Low returns in a rising interest rate environment |

| Variable Annuity | Investment returns linked to underlying assets, potential for growth | Potential for higher returns, tax-deferred growth | Market risk, potential for principal loss |

| Indexed Annuity | Returns linked to a specific index, such as the S&P 500 | Potential for higher returns, downside protection | Limited upside potential, may not keep pace with inflation |

| Immediate Annuity | Payments begin immediately upon purchase | Instant income stream, guaranteed payments | Limited flexibility, may not be suitable for long-term goals |

| Deferred Annuity | Payments begin at a later date, allowing for growth | Tax-deferred growth, potential for higher returns | Longer waiting period, potential for market risk |

Annuity Bond Investment Strategies: Is Annuity Bond 2024

Investing in annuity bonds requires careful consideration of your financial goals, risk tolerance, and investment horizon. Different strategies can be employed to maximize the benefits and minimize the risks associated with these investments.

An annuity is a financial product often used for retirement income. You can find out more about how annuities are used here. The metaverse is a rapidly growing field, and Android app development for the metaverse is becoming increasingly important.

Strategies for Annuity Bond Investments

Here are some common investment strategies for annuity bonds:

- Income Generation:Annuity bonds can be used to generate a steady stream of income, particularly for retirees or those seeking to supplement their income.

- Principal Protection:Annuity bonds offer principal protection, making them suitable for conservative investors who prioritize preserving their capital.

- Tax Planning:Certain types of annuity bonds, such as deferred annuities, can offer tax-deferred growth, allowing for tax-efficient accumulation of wealth.

- Long-Term Growth:Variable annuities, while carrying market risk, can offer potential for long-term growth through investments in equities or other assets.

Factors to Consider

When selecting an annuity bond investment strategy, consider the following factors:

- Investment Goals:Define your financial objectives, such as income generation, principal protection, or growth.

- Risk Tolerance:Assess your willingness to accept potential losses in exchange for higher returns.

- Time Horizon:Determine the length of time you plan to hold the investment.

- Tax Situation:Understand the tax implications of different annuity bond types.

Examples of Annuity Bond Utilization

Annuity bonds can be incorporated into various investment portfolios to achieve specific goals:

- Retirement Planning:Retirees can use annuity bonds to generate a reliable income stream, providing financial security during their golden years.

- Estate Planning:Annuity bonds can be used to create a legacy by providing income for beneficiaries after the bondholder’s death.

- Long-Term Savings:Deferred annuities can serve as a tax-efficient way to save for long-term goals, such as college education or a down payment on a house.

Annuity Bond Regulations and Tax Implications

Investing in annuity bonds is subject to regulations and tax implications that vary depending on the jurisdiction and the specific type of annuity bond. Understanding these aspects is crucial for making informed investment decisions.

Regulations Governing Annuity Bonds

Annuity bonds are regulated by government agencies and insurance departments to protect investors and ensure fair market practices. These regulations may include:

- Financial Strength Requirements:Insurance companies issuing annuity bonds must meet specific financial strength requirements to ensure they can fulfill their obligations to policyholders.

- Disclosure Requirements:Issuers are required to provide comprehensive disclosures about the features, risks, and costs associated with annuity bonds.

- Consumer Protection Laws:Various laws and regulations are in place to protect consumers from fraud and deceptive practices in the annuity bond market.

Tax Implications of Annuity Bonds

The tax treatment of annuity bonds varies depending on the type of annuity and the jurisdiction. Here are some general tax implications:

- Tax-Deferred Growth:Deferred annuities allow for tax-deferred growth, meaning that taxes are not paid on the earnings until they are withdrawn.

- Taxable Income:Payments from annuity bonds are generally considered taxable income, subject to ordinary income tax rates.

- Tax-Free Income:Some types of annuity bonds, such as tax-free annuities, offer tax-free income payments.

Potential Tax Benefits and Drawbacks

Annuity bonds can offer tax advantages, such as tax-deferred growth or tax-free income, but they also have potential tax drawbacks:

- Taxable Withdrawals:When withdrawing funds from an annuity bond, the withdrawals are generally taxable as ordinary income.

- Surrender Charges:Some annuity bonds may impose surrender charges if you withdraw funds before a certain period.

- Tax Penalties:Early withdrawals from an annuity bond before age 59 1/2 may be subject to penalties.

Annuity Bond Risks and Considerations

While annuity bonds offer a degree of security and predictable income, they also come with inherent risks that investors should carefully consider. Understanding these risks is crucial for making informed investment decisions.

Sharing files between Android and iOS devices can be a hassle, but Pushbullet 2024 simplifies the process. The latest Snapdragon chipsets are also being optimized for gaming, as you can see with the Snapdragon 2024 for gaming phones.

Risks Associated with Annuity Bonds, Is Annuity Bond 2024

Here are some key risks associated with investing in annuity bonds:

- Interest Rate Risk:Fixed annuity bonds can lose value if interest rates rise, as their fixed interest payments become less attractive compared to new investments with higher rates.

- Market Risk:Variable annuities, which are linked to underlying assets, are subject to market risk, meaning that the value of the investment can fluctuate with market conditions.

- Inflation Risk:Fixed annuity payments may not keep pace with inflation, reducing the purchasing power of the income stream over time.

- Credit Risk:The financial strength of the insurance company issuing the annuity bond is crucial, as a decline in the issuer’s creditworthiness could affect the payment of benefits.

- Liquidity Risk:Annuity bonds are generally not as liquid as other investments, meaning that it may be difficult to sell them quickly or at a desired price.

Potential Downsides and Drawbacks

In addition to the risks mentioned above, annuity bonds have some potential downsides and drawbacks:

- Limited Upside Potential:Fixed annuity bonds typically offer limited upside potential, as their returns are fixed and may not keep pace with market growth.

- Surrender Charges:Some annuity bonds impose surrender charges if you withdraw funds before a certain period, which can erode your returns.

- Complex Features:Annuity bonds can have complex features and terms, which may be difficult to understand for some investors.

Factors Affecting Annuity Bond Performance

Several factors can influence the performance of annuity bonds:

- Interest Rates:Interest rates have a significant impact on fixed annuity bond returns, as they determine the fixed interest payments.

- Market Volatility:Variable annuities are subject to market volatility, which can affect their value and returns.

- Inflation:Inflation can erode the purchasing power of annuity payments, especially in the case of fixed annuities.

- Issuer’s Financial Strength:The financial strength of the insurance company issuing the annuity bond is crucial, as a decline in creditworthiness could affect the payment of benefits.

Annuity Bond Providers and Market Trends

The annuity bond market is characterized by a range of providers, each with its own offerings and market presence. Understanding the key providers and market trends is important for investors seeking to navigate this segment of the investment landscape.

While the metaverse presents exciting opportunities, there are also challenges of Android app development to consider. Annuities can also be a complex financial product, and it’s important to understand that an annuity is a life insurance product.

Key Providers of Annuity Bonds

Annuity bonds are primarily issued by insurance companies, which are regulated by state insurance departments. Some of the key providers of annuity bonds in the market include:

- AIG:American International Group, Inc. is a leading global insurance and financial services company that offers a range of annuity products.

- Prudential Financial:Prudential Financial, Inc. is a major financial services company that provides annuity products, including fixed, variable, and indexed annuities.

- MetLife:MetLife, Inc. is a global insurance company that offers a comprehensive suite of annuity products, catering to diverse investor needs.

- New York Life:New York Life Insurance Company is a mutual life insurance company that provides a range of annuity products, including fixed, variable, and indexed annuities.

- Northwestern Mutual:Northwestern Mutual is a mutual life insurance company that offers a range of annuity products, including fixed, variable, and indexed annuities.

Market Trends for Annuity Bonds

The annuity bond market is subject to various trends and influences:

- Low Interest Rate Environment:In a low interest rate environment, fixed annuity bonds may offer lower returns, making variable or indexed annuities more attractive to some investors.

- Aging Population:The aging population is driving demand for annuity products, as individuals seek guaranteed income streams during retirement.

- Regulatory Changes:Regulatory changes, such as those related to capital requirements or consumer protection, can impact the annuity bond market.

- Innovation in Product Design:Insurance companies are constantly innovating and developing new annuity products to meet evolving investor needs.

Factors Influencing Demand for Annuity Bonds

Several factors influence the demand for annuity bonds:

- Interest Rates:Interest rates have a significant impact on the attractiveness of fixed annuity bonds, as higher rates can lead to lower returns.

- Economic Conditions:Economic uncertainty and market volatility can drive demand for annuity products, as investors seek guaranteed income streams and principal protection.

- Retirement Planning:The growing need for retirement income security is driving demand for annuity products, particularly among retirees and pre-retirees.

- Financial Literacy:Increased financial literacy among investors can lead to greater awareness of annuity products and their potential benefits.

Case Studies and Examples

Real-world examples and case studies can provide insights into the practical applications and outcomes of investing in annuity bonds. These examples can illustrate the potential benefits and risks associated with these investments.

Case Study: Retirement Income Generation

A retired individual, aged 65, seeks a guaranteed income stream to supplement their retirement savings. They invest in a fixed annuity bond with a guaranteed annual payment of $10,000 for 20 years. This provides them with a reliable and predictable source of income during their retirement years, offering financial security and peace of mind.

Staying connected is easier than ever with apps like Pushbullet 2024 , which allows you to send notifications from your computer to your phone.

Case Study: Long-Term Savings

A young professional, aged 30, decides to invest in a deferred annuity to save for their child’s college education. They contribute a lump-sum payment of $20,000 to the annuity, which grows tax-deferred over time. When their child is ready for college, they can withdraw the accumulated funds to cover tuition and expenses, benefiting from tax-efficient growth.

Example: Estate Planning

An individual with a large estate wants to provide a legacy for their family. They purchase an annuity bond that will provide a regular income stream to their beneficiaries after their death. This ensures that their loved ones will receive a steady income, even after their passing.

Security is paramount in today’s digital landscape. The Snapdragon 2024 security features are designed to protect your data and privacy. For any Android phone issues, you can check out the Android Authority 2024 Android phone troubleshooting guide for solutions.

Example: Income Protection

A self-employed individual wants to protect their income in case of an unexpected illness or disability. They purchase an income protection annuity that provides a guaranteed monthly payment if they are unable to work. This provides financial security and peace of mind, knowing that their income will be protected during a difficult time.

When it comes to task management, Google Tasks is a popular choice. You can find a comparison of Google Tasks to other task management apps here. For those who enjoy creating digital avatars, Dollify 2024 offers new features to explore.

Summary

Investing in annuity bonds requires careful consideration of your individual financial goals, risk tolerance, and time horizon. By understanding the nuances of these instruments, you can make informed decisions and potentially harness the benefits of annuity bonds to achieve your financial objectives.

This guide serves as a starting point for your journey into the world of annuity bonds, providing a foundation for further exploration and research.

Common Queries

What are the tax advantages of annuity bonds?

Annuity bonds often offer tax advantages, such as tax-deferred growth on earnings and potential tax-free income distributions. However, tax implications can vary depending on the specific type of annuity bond and your individual tax situation. It’s crucial to consult with a tax professional to understand the tax implications of investing in annuity bonds.

Are annuity bonds FDIC insured?

Annuity bonds are not typically FDIC insured. However, some annuity contracts may be backed by insurance companies that are rated highly by independent agencies, providing a level of security. It’s important to research the financial stability and reputation of the issuer before investing in an annuity bond.

What are the risks associated with annuity bonds?

Annuity bonds, like any investment, carry inherent risks. These can include the risk of principal loss, interest rate risk, and the potential for the issuer to default on its obligations. It’s essential to carefully assess these risks and understand your potential exposure before investing in annuity bonds.