What happens if I contribute more than the Roth IRA limit in 2024? This question arises for many individuals seeking to maximize their retirement savings. While the Roth IRA offers tax-free withdrawals in retirement, exceeding the annual contribution limit can lead to penalties and tax implications.

Understanding these consequences is crucial for ensuring your retirement savings remain on track.

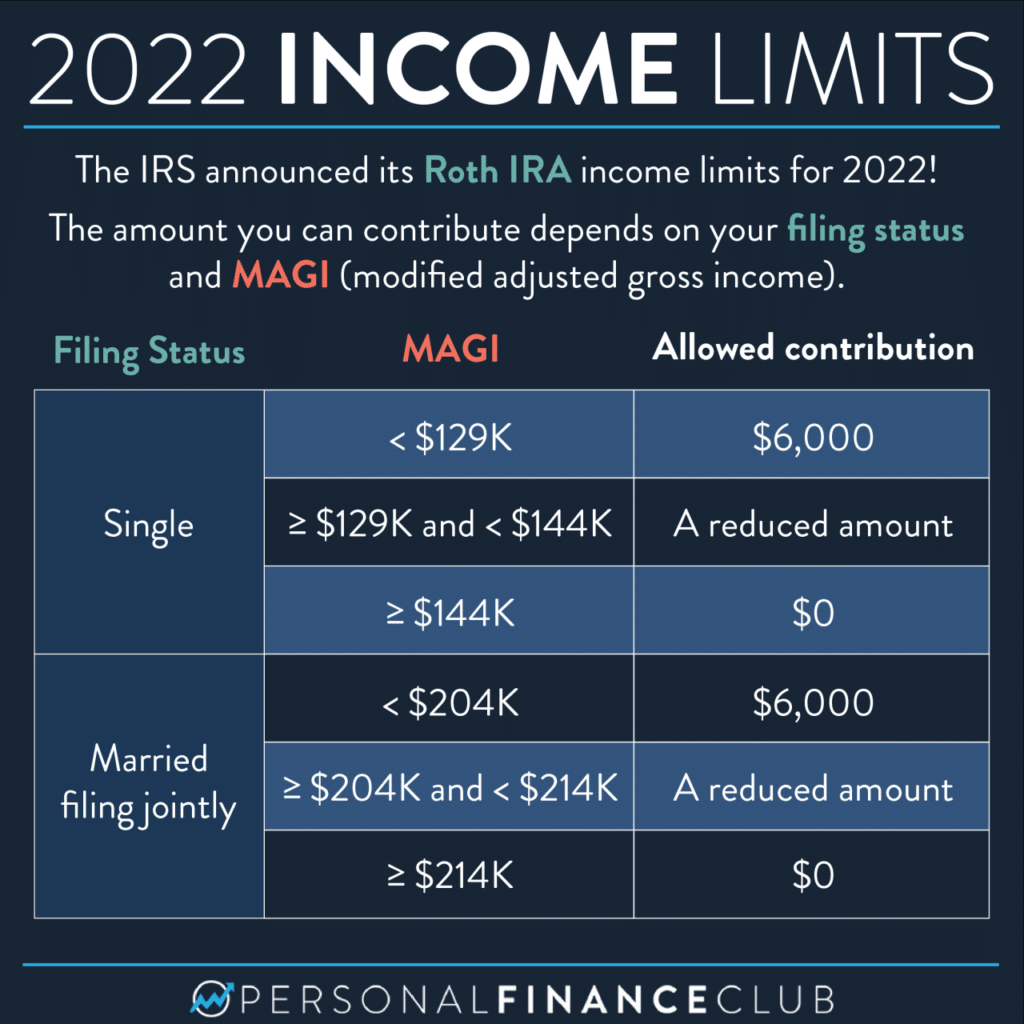

The Roth IRA contribution limit for 2024 is $6,500 for individuals under 50 and $7,500 for those 50 and older. Contributing more than this limit can result in penalties, including a 6% excise tax on the excess contribution. This penalty can significantly impact your retirement savings, so it’s essential to stay within the contribution limits.

Contents List

Understanding the Roth IRA Limit

The Roth IRA is a popular retirement savings plan that allows you to contribute after-tax dollars, grow your investments tax-free, and withdraw your money tax-free in retirement. To maximize your tax advantages, it is important to understand the contribution limits and the consequences of exceeding them.

Contribution Limit for 2024

The contribution limit for a Roth IRA in 2024 is $7,500. This means that you can contribute up to $7,500 to your Roth IRA in 2024, regardless of your income. If you are 50 or older, you can contribute an additional $1,500 as a “catch-up” contribution, bringing your total contribution limit to $9,000.

If you’re planning to contribute to your traditional 401(k) in 2024, it’s good to know the contribution limits. You can find out how much you can contribute in 2024 by checking out the 401k contribution limits for 2024 for traditional 401k.

This information will help you make informed decisions about your retirement savings.

Consequences of Exceeding the Limit

If you contribute more than the annual Roth IRA contribution limit, the IRS will consider the excess contribution as a nondeductible contribution. This means that the excess contribution will not be taxed when you withdraw it in retirement, but it will also not grow tax-free.

Tax Implications of Exceeding the Limit

The IRS will assess a 6% penalty on the excess contribution each year that it remains in your account. This penalty applies to the excess contribution plus any earnings on the excess contribution. You have until the due date of your tax return (including extensions) to withdraw the excess contribution and avoid the penalty.

It’s always good to be aware of the federal tax brackets and personal exemption. The 2024 federal tax brackets and personal exemption page provides detailed information on these topics. Understanding these aspects of the tax code can help you make informed decisions about your financial planning.

If you do not withdraw the excess contribution, the penalty will continue to apply until the excess contribution is withdrawn.

Excess Contribution Penalties

If you contribute more than the Roth IRA limit in 2024, you’ll face penalties. The IRS considers excess contributions as taxable income in the year you make them, and you’ll also pay a penalty on the excess amount.

Penalty Rate

The penalty for exceeding the Roth IRA limit is 6% of the excess contribution. This penalty applies each year the excess contribution remains in the account.

If you’re married filing separately and considering a Roth IRA, knowing the contribution limits is essential. You can find the specific limit for your situation on the What is the Roth IRA contribution limit for 2024 for married filing separately page.

This information will help you make informed decisions about your retirement savings strategy.

Penalties Associated with Exceeding the Limit, What happens if I contribute more than the Roth IRA limit in 2024

Here’s a breakdown of the penalties you might face:

- Tax on Excess Contributions:The IRS considers excess contributions as taxable income in the year you make them. This means you’ll have to pay taxes on the excess amount, potentially increasing your tax liability for the year.

- 6% Penalty on Excess Contributions:In addition to taxes, you’ll also have to pay a 6% penalty on the excess contribution amount. This penalty applies each year the excess contribution remains in the account.

- Potential for Additional Penalties:If you don’t correct the excess contribution within a certain timeframe, you might face additional penalties. The IRS has specific rules and procedures for correcting excess contributions. It’s essential to understand these rules and take the necessary steps to avoid further penalties.

If you have a disability, you may be eligible for a higher standard deduction. To learn more about the standard deduction for people with disabilities in 2024, visit the Standard deduction for people with disabilities in 2024 page. This information can help you maximize your tax benefits and plan your finances effectively.

Impact on Retirement Savings

Excess contribution penalties can significantly impact your retirement savings. Not only will you lose money to taxes and penalties, but you’ll also miss out on the potential growth of the excess contribution over time.

The Roth IRA contribution limit can vary based on your age. To find out the specific limit for your age group, you can check out the Roth IRA contribution limits for 2024 by age page. This information will help you understand how much you can contribute and plan your retirement savings accordingly.

For example, if you contribute $7,500 to your Roth IRA in 2024, exceeding the limit by $1,000, you’ll owe taxes and a 6% penalty on the $1,000. This means you’ll lose $60 in penalties and potentially more in taxes, depending on your tax bracket.

Rectifying Excess Contributions

Don’t panic if you’ve contributed more than the Roth IRA limit for 2024. You have options to fix this situation and avoid penalties. The IRS allows you to remove excess contributions and related earnings to avoid penalties.

Removing Excess Contributions

You can remove excess contributions from your Roth IRA to avoid penalties. This process involves withdrawing the excess contribution amount and any earnings associated with it. You can choose to withdraw the excess contribution and earnings before the tax filing deadline for the year in which the excess contribution was made, or you can choose to withdraw them by the tax filing deadline for the following year.Here are the steps involved:* Contact your Roth IRA provider:Inform them about the excess contribution and request a withdrawal.

Specify the excess amount

If you’re planning to contribute to your 401(k) in 2024, you’ll want to know the contribution limit. You can find this information on the What is the 401k contribution limit for 2024 page. This knowledge will help you maximize your contributions and plan for a comfortable retirement.

Clearly state the amount you wish to withdraw.

Choose withdrawal method

Decide whether to withdraw the excess contribution and earnings as a lump sum or in installments.

Complete necessary paperwork

The contribution limits for IRAs can change from year to year. To compare the limits for 2024 and 2023, you can visit the Ira contribution limits for 2024 vs 2023 page. This comparison will help you understand the latest changes and adjust your retirement savings plan accordingly.

Sign the required forms for the withdrawal.

Timeline for Removing Excess Contributions

The timeline for removing excess contributions is crucial to avoid penalties. Here’s a breakdown:* Before the tax filing deadline:You have until the tax filing deadline for the year in which the excess contribution was made to remove it and avoid penalties. For example, if you made an excess contribution in 2024, you have until April 15, 2025, to remove it.

When it comes to maximizing your 401(k) contributions, it’s helpful to know the maximum limit. The What is the maximum 401k contribution for 2024 page provides this information, which can help you plan your retirement savings effectively.

By the tax filing deadline of the following year

If you miss the deadline for the current year, you can still remove the excess contribution and earnings by the tax filing deadline of the following year. However, you may be subject to a 6% penalty on the excess contribution.

Want to know how much you can contribute to your 401(k) in 2024 after taxes? You can find the answer to this question by visiting the How much can I contribute to my 401k in 2024 after taxes page.

Understanding these limits can help you plan your retirement savings strategy.

Avoiding Future Excess Contributions

To avoid future excess contributions, consider these strategies:* Track your contributions:Keep a record of your Roth IRA contributions throughout the year.

Stay informed about annual limits

Be aware of the annual contribution limits and adjust your contributions accordingly.

Consider a Roth IRA calculator

For those considering a Roth IRA, it’s important to understand the contribution limits. You can find the latest information on the Roth IRA contribution limits for 2024. This knowledge will help you make informed decisions about your retirement savings strategy.

Utilize online tools to help you calculate your contributions and avoid exceeding the limit.

Consult a financial advisor

Seek guidance from a qualified financial professional to help you manage your Roth IRA contributions effectively.

Alternatives to a Roth IRA

If you’ve hit the Roth IRA contribution limit for 2024 and are still looking for ways to save for retirement, don’t worry! There are several other retirement savings options available. These alternatives offer various benefits and features, allowing you to choose the best fit for your financial goals and circumstances.

Traditional IRA

Traditional IRAs offer tax-deductible contributions, meaning you can deduct your contributions from your taxable income, potentially lowering your tax bill in the present. However, you’ll pay taxes on withdrawals in retirement. Traditional IRAs are a great option if you expect to be in a lower tax bracket in retirement than you are now.

This is because you’ll pay taxes on your withdrawals at your lower retirement tax rate, rather than your current higher tax rate.

If you’re looking to contribute to a Roth 401(k) in 2024, you’ll want to be aware of the contribution limits. You can find the details on the 401k contribution limits for 2024 for Roth 401k page. Understanding these limits will help you maximize your contributions and plan for a comfortable retirement.

401(k)

A 401(k) is a retirement savings plan offered by your employer. It allows you to contribute pre-tax dollars, reducing your taxable income. Like traditional IRAs, withdrawals in retirement are taxed. Many employers offer matching contributions, which means they’ll contribute a certain percentage of your salary to your 401(k) account, boosting your retirement savings.

If you’re a head of household considering a Roth IRA, you’ll want to know the contribution limit for your filing status. You can find this information on the Roth IRA contribution limit 2024 for head of household page. This information will help you make informed decisions about your retirement savings strategy.

Other Retirement Plans

Beyond traditional IRAs and 401(k)s, there are other retirement savings options available, including:

- Solo 401(k): This plan is for self-employed individuals and small business owners. It allows you to contribute both as an employee and an employer, potentially maximizing your retirement savings.

- SEP IRA: A SEP IRA is a simplified retirement plan for self-employed individuals and small business owners. It allows you to contribute a percentage of your net earnings, up to a certain limit.

- SIMPLE IRA: This plan is for small businesses with 100 or fewer employees. It offers both employee and employer contributions, with a simple contribution structure.

- Defined Benefit Plan: These plans provide a guaranteed retirement income based on your salary and years of service. They are typically offered by larger companies.

Comparison of Retirement Accounts

Here’s a table comparing the key features and benefits of different retirement accounts:

| Account Type | Contribution Limit | Tax Deductibility | Taxation at Withdrawal | Other Benefits |

|---|---|---|---|---|

| Roth IRA | $6,500 (2024) | Non-deductible | Tax-free | Potential for tax-free growth and withdrawals in retirement |

| Traditional IRA | $6,500 (2024) | Deductible | Taxable | Potential for tax savings in the present |

| 401(k) | $22,500 (2024) | Deductible | Taxable | Employer matching contributions |

| Solo 401(k) | $66,000 (2024) | Deductible | Taxable | High contribution limits for self-employed individuals |

| SEP IRA | 25% of net earnings | Deductible | Taxable | Simplified contribution structure for self-employed individuals |

| SIMPLE IRA | $15,500 (2024) | Deductible | Taxable | Employer matching contributions |

| Defined Benefit Plan | N/A | N/A | Taxable | Guaranteed retirement income |

Tax Implications of Excess Contributions

Contributing more than the annual Roth IRA limit can have significant tax consequences. The IRS considers excess contributions as taxable income in the year you made them. You’ll also face a 6% penalty on the excess amount, which can be compounded annually until the excess is removed.

Penalties and Taxes on Excess Contributions

Excess contributions are treated as taxable income in the year they were made. This means you’ll have to pay taxes on the excess amount, as well as any earnings on those contributions, at your current tax rate.

- Tax Rate:You’ll be taxed on the excess contributions at your ordinary income tax rate.

- Penalty:You’ll also face a 6% penalty on the excess contribution amount. This penalty is applied annually until the excess contribution is withdrawn.

For example, if you contributed $7,000 to your Roth IRA in 2024, exceeding the limit of $6,500, you’ll be taxed on the $500 excess amount at your ordinary income tax rate. You’ll also have to pay a 6% penalty on the $500 excess, which is $30.

Impact on Future Tax Liabilities

Excess contributions can also affect your future tax liabilities. If you fail to remove the excess contributions and the associated earnings before the tax filing deadline for the following year, the penalty can increase to 10% of the excess contributions.

Additionally, the excess contributions can impact your future Roth IRA contributions, as they are considered part of your total contribution history.

Minimizing Tax Implications

You can minimize the tax implications of excess contributions by taking the following steps:

- Withdraw the excess contributions:The best way to avoid penalties is to withdraw the excess contributions as soon as you realize you’ve overcontributed.

- Withdraw the excess contributions and earnings:If you’ve already earned interest or dividends on the excess contributions, you’ll need to withdraw both the excess contributions and the earnings.

- Consider a Traditional IRA:If you’re over the Roth IRA contribution limit, consider a Traditional IRA instead. Traditional IRA contributions are tax-deductible, meaning you can deduct the contributions from your taxable income, reducing your tax liability in the current year. However, you’ll have to pay taxes on the distributions when you withdraw the money in retirement.

Long-Term Considerations: What Happens If I Contribute More Than The Roth IRA Limit In 2024

While the immediate consequence of exceeding the Roth IRA limit is a penalty, the long-term impact on your retirement savings can be significant. Understanding these potential effects is crucial for making informed decisions about your retirement planning.

Impact on Retirement Savings

Exceeding the Roth IRA limit can negatively impact your retirement savings in several ways. Firstly, you may miss out on the opportunity to contribute more to your retirement accounts, potentially limiting your overall savings. Secondly, the penalties associated with excess contributions can eat into your retirement funds, reducing the amount available for your golden years.

Tax season is around the corner, and using a tax calculator can be helpful. To get a head start on your tax planning, check out the How to use a tax calculator for October 2024. This guide will help you understand the basics of using a tax calculator and how it can benefit you.

Impact on Tax Planning and Retirement Income

Excess contributions can also affect your tax planning and retirement income. The penalties associated with exceeding the limit can increase your tax burden, making it harder to manage your finances during retirement. Furthermore, exceeding the limit can impact your eligibility for certain tax benefits, such as tax deductions or credits, which can further affect your overall tax planning strategy.

When it comes to saving for retirement, an IRA can be a valuable tool. For those interested in traditional IRAs, the Ira contribution limits for traditional IRA in 2024 are an important factor to consider. Understanding these limits can help you maximize your contributions and potentially lower your tax liability.

Strategies for Managing Retirement Savings After Exceeding the Roth IRA Limit

If you have exceeded the Roth IRA limit, there are strategies you can use to manage your retirement savings.

- Withdraw the excess contribution: This is the simplest way to rectify the situation. You can withdraw the excess contribution, along with any associated earnings, before the tax filing deadline for the year. This option allows you to avoid penalties, but you will not benefit from the tax-free growth of the withdrawn funds.

If you’re considering a Roth IRA, knowing the contribution limits is crucial. You can find the latest information on the Roth IRA contribution limits for 2024. This knowledge will help you make informed decisions about your retirement savings strategy.

- Rollover the excess contribution to a traditional IRA: If you don’t want to withdraw the excess contribution, you can roll it over to a traditional IRA. This will avoid penalties, but you will need to pay taxes on the funds when you withdraw them in retirement.

- Consider other retirement savings options: If you have already maxed out your Roth IRA and are still looking to save for retirement, consider other options such as a 401(k), 403(b), or SEP IRA. These accounts may have higher contribution limits, allowing you to save more for retirement.

Closing Summary

Exceeding the Roth IRA contribution limit can have significant consequences for your retirement savings. Understanding the penalties and tax implications associated with excess contributions is crucial for avoiding potential financial setbacks. If you find yourself in this situation, taking immediate steps to rectify the excess contributions is essential.

Remember, planning and staying informed about your retirement savings options can help you navigate the complexities of retirement planning and maximize your long-term financial well-being.

Helpful Answers

Can I withdraw the excess contributions from my Roth IRA to avoid penalties?

Yes, you can withdraw excess contributions from your Roth IRA to avoid penalties. You must withdraw the excess contribution, along with any earnings on the excess contribution, by the tax filing deadline for the year following the year of the excess contribution.

For example, if you made an excess contribution in 2024, you would need to withdraw the excess contribution and earnings by April 15, 2025.

What if I don’t have enough money to withdraw the excess contributions?

If you don’t have enough money to withdraw the excess contributions, you can request a waiver from the IRS. However, the IRS will only grant a waiver if you can demonstrate that the excess contribution was due to a reasonable error, such as a mistake in calculating your income.

What are some alternative retirement savings options if I exceed the Roth IRA limit?

If you exceed the Roth IRA limit, you can consider alternative retirement savings options, such as a traditional IRA, a 401(k), or a Solo 401(k). These options have different contribution limits and tax implications, so it’s essential to research and compare them before making a decision.